The world of business and legal transactions is experiencing a profound transformation, and one of the most innovative changes, in particular, is the rise of blockchain-based smart contracts. These self-executing contracts, with the terms of the agreement directly written into code, have the potential to fundamentally redefine how legal agreements are made, enforced, and executed. Dubai, known for its progressive and tech-forward mindset, has, therefore, been at the forefront of embracing blockchain technology, including smart contracts, within its legal framework.

This article, consequently, delves into the concept of blockchain-based smart contracts, their legal recognition in Dubai, and how the Dubai legal framework for smart contracts is evolving to provide a seamless and secure ecosystem for businesses and individuals.

Understanding Blockchain-Based Smart Contracts

Before diving into the legal recognition of smart contracts in Dubai, it’s essential to understand the technology itself. A smart contract is a computer protocol that automatically enforces the terms of an agreement. Once predefined conditions are met, the contract self-executes without requiring manual intervention, third-party oversight, or mediation. This automation results in faster, cheaper, and more secure transactions.

Blockchain technology builds smart contracts on a decentralized ledger system that ensures transparency, immutability, and security. When someone creates a smart contract, they deploy it to the blockchain, where it becomes part of an unchangeable record. This makes the contract tamper-proof, ensuring that once the parties agree on the terms, they cannot alter or delete them without everyone’s consensus.

Key Features of Blockchain-Based Smart Contracts

- Automation: Once the conditions are met, the contract automatically executes, eliminating the need for intermediaries.

- Security: Blockchain’s encryption and decentralization ensure that smart contracts are secure and cannot be tampered with.

- Transparency: All parties involved can see the contract’s terms and track its execution in real-time.

- Cost Efficiency: By eliminating the need for third-party intermediaries, smart contracts reduce costs associated with legal and administrative processes.

The Rise of Smart Contracts in Dubai

Dubai has approved its first law to regulate #crypto assets. #cryptocurrency #bitcoin $BTC https://t.co/vm61RRdZj0

— Bitcoin.com News (@BTCTN) March 11, 2022

Dubai, with its forward-thinking approach and vision of becoming a global leader in innovation, has been at the forefront of integrating blockchain technology into its legal and business infrastructure. The city has laid out ambitious plans to adopt blockchain across all sectors, including legal services, and smart contracts are one of the key areas of focus.

Dubai’s Commitment to Blockchain

Dubai’s government has made significant strides toward blockchain adoption, especially through the Dubai Blockchain Strategy, which was launched in 2016. This strategy aims to position Dubai as the first city fully powered by blockchain by 2020. The Dubai Future Foundation and the Dubai Blockchain Center have played a key role in supporting blockchain startups and integrating this technology into various government sectors.

In 2018, Dubai introduced its Smart Dubai Initiative, focusing on transforming the city into the world’s smartest and most efficient city by harnessing the power of blockchain and other advanced technologies. This initiative aligns with Dubai’s broader mission of improving government efficiency, reducing costs, and increasing transparency. Smart contracts are central to this vision, as they can streamline government processes, reduce bureaucracy, and enhance the efficiency of both private and public sector transactions.

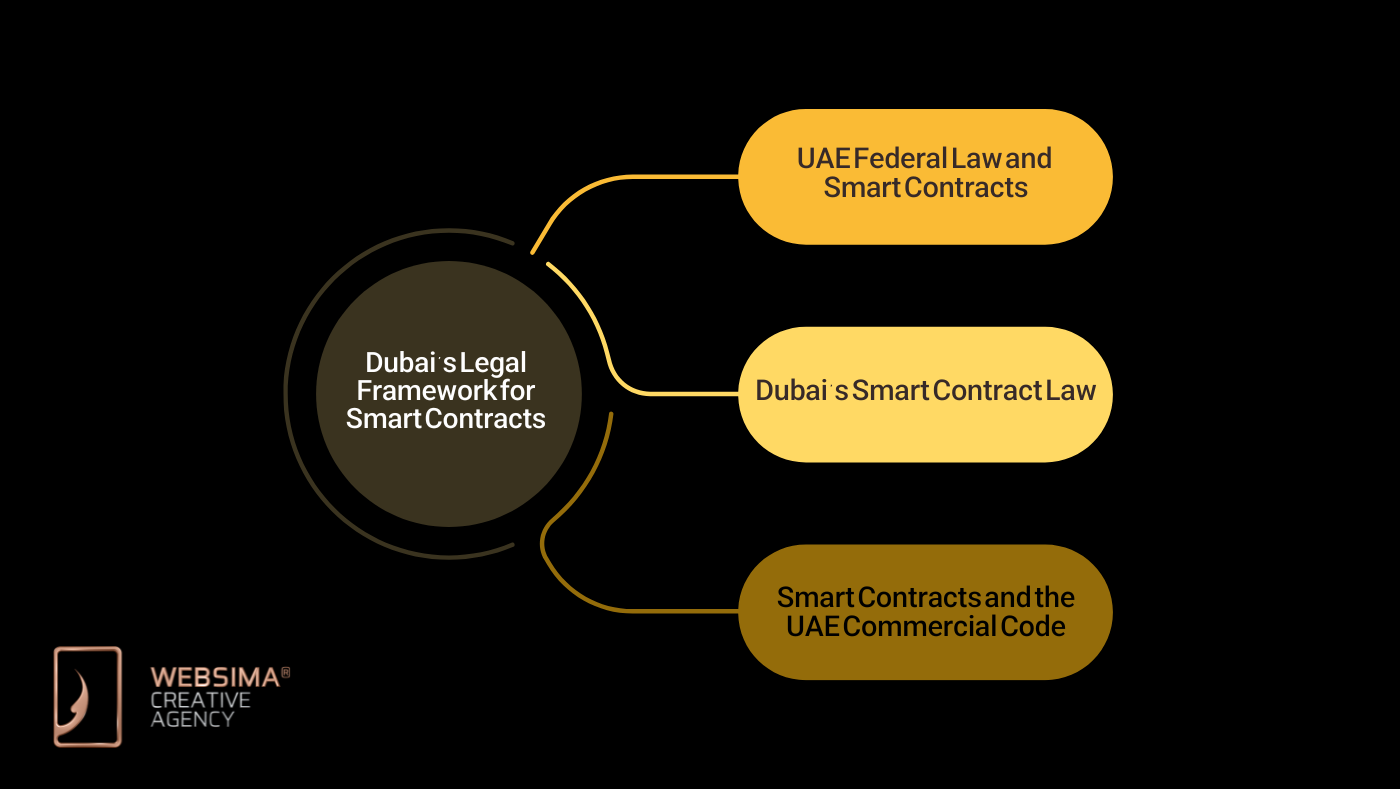

Dubai’s Legal Framework for Smart Contracts

One of the critical components of the widespread adoption of smart contracts is the legal recognition of these contracts. In many countries, the use of blockchain and smart contracts has raised concerns about their legal enforceability, given that these contracts are often entirely digital and do not involve traditional legal intermediaries. However, Dubai’s legal framework for smart contracts is uniquely positioned to support the use of blockchain technology for legal purposes which makes blockchain’s role in attracting foreign investment to Dubai, pivotal.

1. UAE Federal Law and Smart Contracts

The UAE has been proactive in establishing a legal framework that recognizes blockchain and smart contracts as valid tools for business transactions.

The law emphasizes the use of blockchain technology for government processes, financial services, and business transactions, which directly impacts the use of smart contracts. Although the law does not provide detailed provisions specific to smart contracts, it establishes the groundwork for their legal use by recognizing blockchain as a legitimate and secure technology for record-keeping and transaction execution.

2. Dubai’s Smart Contract Law

Dubai has taken additional steps to integrate smart contracts into its legal framework. Dubai International Financial Centre (DIFC) is one of the city’s leading financial free zones. Considering DIFC’s role in web3 and blockchain adoption in Dubai, DIFC has introduced a legal framework for smart contracts in order to govern the use of digital assets and blockchain technology within its jurisdiction. The framework makes smart contracts legally enforceable in the DIFC, setting a precedent for the broader acceptance of blockchain-based agreements.

Under the DIFC’s laws, authorities recognize smart contracts as valid and enforceable, provided the following conditions are met:

- The contract must clearly and unambiguously state its terms.

- The parties must automate the contract’s execution and performance through code, with the blockchain serving as the trusted and verified record.

- The parties must consent to the terms, which they can do digitally.

3. Smart Contracts and the UAE Commercial Code

The UAE has adapted the Commercial Code and other related commercial laws to accommodate blockchain and digital transactions. These laws focus on ensuring that digital contracts and records, including those executed through smart contracts, hold the same legal weight as traditional paper-based agreements. This recognition is crucial in industries like finance, real estate, and insurance, where contracts and agreements are essential to business operations.

In the UAE, lawmakers are updating the Commercial Transactions Law (Federal Law No. 18 of 1993) and other related legislation to account for the increased role of digital transactions and smart contracts. While the full integration of blockchain into these laws is still evolving, the recognition of digital signatures and smart contract automation under existing commercial law is paving the way for smoother adoption.

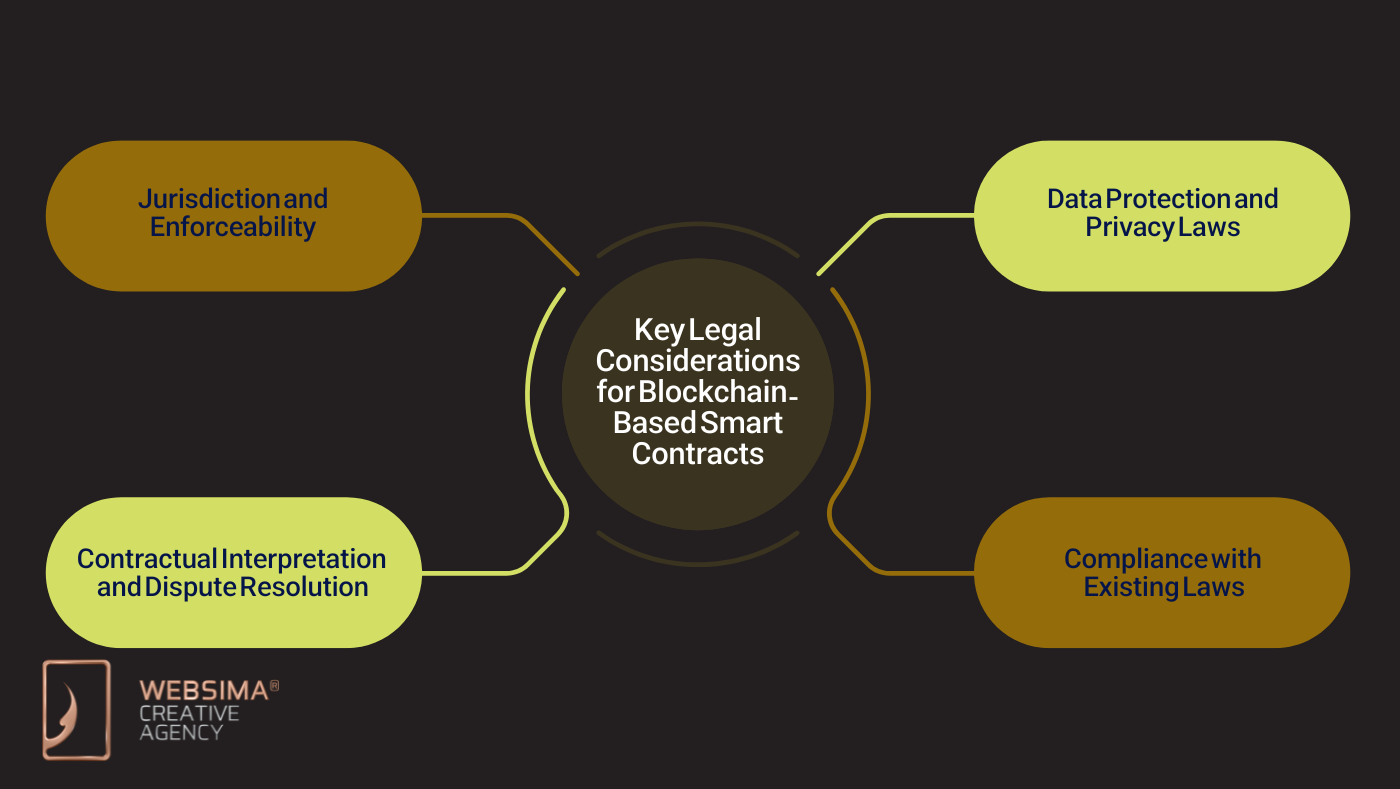

Key Legal Considerations for Blockchain-Based Smart Contracts

For businesses looking to leverage blockchain-based smart contracts in Dubai, there are several important legal considerations to keep in mind:

1. Jurisdiction and Enforceability

While Dubai and the UAE have made significant strides in legal recognition, businesses using smart contracts should always consider jurisdictional issues. Smart contracts, by their nature, can involve parties from different countries. It’s essential to understand how authorities will enforce cross-border transactions and whether the Dubai legal framework applies to international agreements executed via smart contracts.

In Dubai, smart contracts typically fall under the specific laws of the Emirate, and DIFC regulations govern contracts executed within the DIFC. However, it’s crucial to ensure that the terms of the contract are clear and specify which jurisdiction will govern any disputes.

2. Data Protection and Privacy Laws

As smart contracts involve the exchange of personal and business data, it’s essential to comply with data protection and privacy laws. In Dubai, the UAE Data Protection Law, along with the General Data Protection Regulation (GDPR) for businesses that deal with EU residents, requires companies to handle personal data responsibly. While blockchain technology is secure, businesses must manage it in a way that respects privacy laws, especially since data stored on the blockchain is immutable.

3. Contractual Interpretation and Dispute Resolution

One of the challenges with smart contracts is that they automate processes and rely on code, leaving little room for interpretation in case of disputes. Legal systems around the world, including in Dubai, are adapting to provide mechanisms for resolving disputes arising from smart contracts.

In Dubai, smart contracts in the DIFC are subject to the DIFC Courts for arbitration and resolution of legal disputes. As the legal landscape continues to evolve, businesses will need to carefully structure their contracts to address potential issues, such as bugs in the code or ambiguities in the contract’s terms.

4. Compliance with Existing Laws

While the UAE’s legal framework supports blockchain and smart contracts, it’s important to ensure that businesses comply with all other relevant regulations. This includes compliance with anti-money laundering (AML) and counter-terrorism financing (CTF) laws, particularly in sectors like finance, real estate, and cryptocurrency, which often use smart contracts.

The Future of Blockchain-Based Smart Contracts in Dubai

Dubai’s legal framework for blockchain-based smart contracts is evolving, and the future looks promising. As the UAE continues to push forward with its digital transformation goals, we can, therefore, expect to see further refinements in the legal recognition and regulation of smart contracts.

Moreover, blockchain-based smart contracts offer significant benefits, including efficiency, cost reduction, and security. These benefits, in turn, make them particularly attractive to businesses in Dubai, which is home to a dynamic and diverse economy. As the legal framework continues to develop, smart contracts will, undoubtedly, play an increasingly important role in driving innovation and business transformation in the UAE.

Conclusion

Blockchain-based smart contracts represent a significant leap forward in the way agreements are executed, monitored, and enforced. In this context, Dubai’s legal framework for smart contracts is among the most progressive in the world, offering businesses the legal certainty needed to embrace this transformative technology. Furthermore, with the Dubai Blockchain Strategy and the DIFC’s dedicated legal framework for smart contracts, Dubai is, undoubtedly, well on its way to becoming a global leader in blockchain technology.

Websima, as the leading blockchain service provider in Dubai, is more than happy to help, if you are planning to start a blockchain-based business in Dubai. Blockchain, crypto and web3 web and website development, smart contract programming and development, Blockchain, Web3 and crypto company establishment are just a few out of many services that we provide. Feel free to contact us to book for a free consultation meeting with our talented team.