Table of Contents

- Introduction

- Why CBDC Interoperability Matters in the UAE

- Current UAE Landscape for CBDC and Stablecoins

- Technical Patterns for Interoperability

- API Gateways

- Cross-Chain Bridges

- Layer-2 Settlement Channels

- Developer Strategies for Retail Payments

- Wallet Integration

- Point-of-Sale Compatibility

- Cross-Border Microtransactions

- Developer Strategies for Wholesale Payments

- Interbank Settlement

- Tokenized Securities Integration

- Liquidity Management

- Compliance and Regulatory Architecture

- Infrastructure and Network Models

- Permissioned vs. Public Chains

- Oracle Integration

- Offline Payment Design

- Case Studies and Global Comparisons

- Challenges and Risks

- Outlook for CBDC Interoperability in UAE 2030

- Frequently Asked Questions (FAQs)

- Final Thoughts

- Websima – Building Interoperable Blockchain Payment Systems

Introduction

Central bank digital currencies (CBDCs) are moving rapidly from pilot projects to real-world implementation. For the United Arab Emirates, the Digital Dirham is at the heart of its financial modernization strategy. Alongside, stablecoins—particularly fiat-backed tokens—are emerging as indispensable rails for programmable payments.

Unless CBDCs and stablecoins can interoperate, the UAE’s ecosystem risks fragmentation. That is why CBDC interoperability UAE is a pressing challenge for developers, regulators, and financial institutions. By building bridges between these systems, the UAE can accelerate adoption and position itself as a leader in global digital finance.

Central Bank of UAE to launch its Digital Dirham CBDC later this year 2025 in Q4.

It will be distributed to “banks, exchanges, finance companies and fintechs.”

To be used for cross border payments, it will need a medium of exchange into other digital currencies. https://t.co/F2ReIoCmUB pic.twitter.com/BGDIxgMgoE

— Chad Steingraber (@ChadSteingraber) March 31, 2025

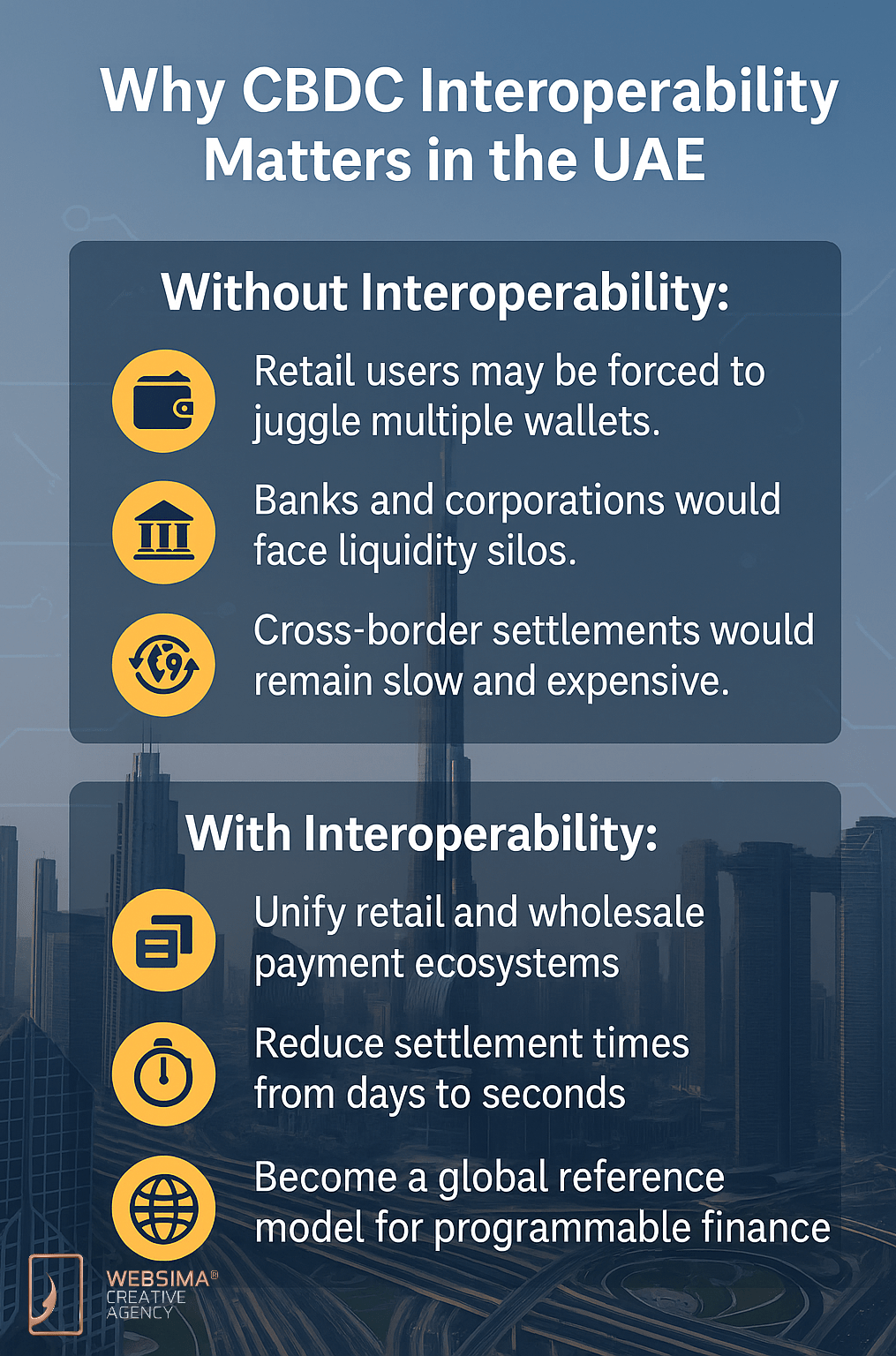

Why CBDC Interoperability Matters in the UAE

The UAE’s economy thrives on cross-border trade, remittances, and financial innovation. Without interoperability:

- Retail users may be forced to juggle multiple wallets.

- Banks and corporations would face liquidity silos.

- Cross-border settlements would remain slow and expensive.

With interoperability, the UAE can:

- Unify retail and wholesale payment ecosystems

- Reduce settlement times from days to seconds

- Become a global reference model for programmable finance

For developers, this creates a high-value design space: building APIs, compliance modules, and wallet integrations that allow seamless money movement across digital forms.

Current UAE Landscape for CBDC and Stablecoins

The Central Bank of the UAE (CBUAE) has issued a detailed policy paper, “Digital Dirham – A Primer on the UAE’s Central Bank Digital Currency (Policy Paper No. 1/2025)”, outlining the framework for its retail and wholesale CBDC pilots (CBUAE).

The UAE government also presents a broader CBDC strategy, confirming that the Digital Dirham will serve cross-border settlements, domestic wholesale transactions, and everyday retail use cases (u.ae).

On the stablecoin side, ADGM’s Financial Services Regulatory Authority (FSRA) recently updated its digital asset regulatory framework, clarifying the rules for fiat-referenced tokens, smooth exchange of fiat currency and crypto currency for UAE users and strengthening governance standards for issuers (ADGM).

Together, these initiatives create a dual system where CBDCs and stablecoins can evolve in tandem—ready for interoperability.

Technical Patterns for Interoperability

API Gateways

APIs provide a practical way for developers to link CBDC and stablecoin networks. By building RESTful endpoints, wallets, exchanges, and banking platforms can seamlessly initiate transfers, check balances, and verify compliance across ledgers. Developers in the UAE should anticipate API standards being issued by the CBUAE for consistency.

Cross-Chain Bridges

Cross-chain interoperability can be achieved through smart contracts that lock CBDC units while issuing wrapped stablecoin tokens—or vice versa. For example, a Digital Dirham could be locked on a permissioned blockchain while a wrapped version circulates on a public chain to facilitate DeFi integration. Security audits of bridge contracts are critical to mitigate risks.

Layer-2 Settlement Channels

Layer-2 protocols allow micropayments to occur off-chain while anchoring settlement back to the CBDC ledger. For retail developers, this reduces congestion, ensures faster UX at point-of-sale, and keeps fees minimal. In a UAE context, this could be integrated into metro cards, toll payments, or small-value cross-border remittances.

Developer Strategies for Retail Payments

Wallet Integration

Wallets that combine CBDCs and stablecoins give users flexibility. Developers can program smart routing so payments automatically use the cheapest rail available. For example, a purchase might default to CBDC domestically but stablecoin when the counterparty is overseas.

Point-of-Sale Compatibility

POS systems must accommodate interoperability by supporting QR codes, NFC, or biometric authorizations tied to both CBDC and stablecoin rails. The opportunity for developers is to create universal payment SDKs and fiat stablecoin currency for UAE merchants, where they can plug into existing terminals.

Cross-Border Microtransactions

The UAE has one of the world’s highest remittance volumes. With CBDC–stablecoin interoperability, a worker in Dubai could send AED instantly to family abroad, automatically converting into a stablecoin pegged to the local currency. This requires developers to integrate liquidity pools and FX oracles into wallet applications.

Developer Strategies for Wholesale Payments

Interbank Settlement

For banks, interoperability means being able to swap liquidity between CBDCs and stablecoins without passing through legacy correspondent networks. Developers can build interbank APIs that allow CBDC balances to offset stablecoin liabilities in near real-time.

Tokenized Securities Integration

Delivery-versus-payment (DvP) requires atomic swaps between a security token and settlement currency. By coding interoperability into CBDC–stablecoin layers, tokenized sukuk or bonds can settle instantly, reducing counterparty risk.

Liquidity Management

Stablecoins are often used as intraday liquidity buffers. Developers can program automated treasury contracts that swap between CBDC holdings and stablecoin liquidity pools, helping banks and corporates optimize capital efficiency while staying within regulatory liquidity ratios.

Compliance and Regulatory Architecture

Interoperability must never compromise oversight. Developers must embed:

- AML/CFT screening in transaction flows

- Programmable compliance logic within smart contracts

- Cross-border reporting APIs to support regulator data access

This ensures that innovation aligns with ADGM, VARA, and CBUAE oversight frameworks.

Infrastructure and Network Models

Permissioned vs. Public Chains

CBDCs will likely operate on permissioned ledgers, while stablecoins may run on public chains such as Ethereum or Stellar. Secure “federated gateways” must be built to connect these environments while maintaining compliance.

Oracle Integration

Accurate oracles are essential for interoperability, particularly for FX rates, settlement finality, and collateral audits. Inaccurate data feeds could lead to systemic risks in multi-chain transactions.

Offline Payment Design

The Digital Dirham aims to include the unbanked. Developers should prioritize offline wallet design—using Bluetooth, NFC, or SMS fallback—to allow transactions even when internet access is limited.

Case Studies and Global Comparisons

- Project mBridge proves that multi-CBDC interoperability can reduce settlement costs and improve transparency in cross-border trade.

- Singapore MAS pilots demonstrate how tokenized deposits and CBDCs can coexist in wholesale settlement.

- European CBDC pilots (e.g., EUROe) show stablecoins acting as bridges for retail adoption while CBDC infrastructure develops.

For UAE developers, the lesson is clear: interoperability should be modular, secure, and tailored to regional use cases such as energy trade, remittances, and sukuk issuance.

Challenges and Risks

- Cybersecurity risks: Cross-chain bridges remain high-value targets for hackers.

- Scalability pressures: Retail-scale interoperability must handle millions of daily transactions.

- Legal clarity: Questions remain on liability when a transaction fails mid-bridge.

- User adoption: Retail consumers may not fully grasp the differences between CBDC and stablecoins, requiring education campaigns.

Outlook for CBDC Interoperability in UAE 2030

By 2030, the UAE will likely operate a multi-rail, interoperable payment system where CBDCs, stablecoins, and tokenized deposits work together seamlessly. The Digital Dirham could act as the settlement backbone, while stablecoins provide liquidity in trade finance and DeFi markets.

For developers, this future means long-term opportunities in:

- Cross-border remittance APIs

- Tokenized market infrastructure

- Compliance middleware solutions

- Wallet ecosystems with CBDC + stablecoin routing

The UAE’s willingness to pilot, regulate, and adapt ensures it will remain a leader in global CBDC interoperability initiatives.

Frequently Asked Questions (FAQs)

Will stablecoins compete with the Digital Dirham?

No. Interoperability ensures they complement each other’s strengths.

Is interoperability live in the UAE now?

Not fully, but pilots like Project mBridge and domestic Digital Dirham tests are progressing.

Which sectors benefit most from Digital Dirham and interoperability?

Remittances, e-commerce, tokenized securities, wholesale banking, and trade finance.

Can developers already build tools?

Yes—within CBUAE and ADGM frameworks, sandboxes encourage developer participation.

Final Thoughts

The UAE’s dual-track strategy—rolling out a CBDC while regulating stablecoins—makes it a pioneer in digital money. With official frameworks now in place, the next step is interoperability. Developers who embrace CBDC interoperability UAE projects today will be at the forefront of the next decade’s financial transformation.

Websima – Building Interoperable Blockchain Payment Systems

At Websima, we specialize in blockchain architecture that connects CBDCs, stablecoins, and tokenized assets. From smart contract development to cross-chain interoperability solutions, our team helps governments, banks, and fintechs design compliant, future-proof payment systems.

If you are exploring CBDC interoperability UAE, we can guide you through technical design, security auditing, and deployment.

Contact Websima today to build the future of programmable money.